At retirement, you need to purchase an annuity. And you have two choices: either a living annuity or a guaranteed annuity. In our previous post, we spoke about LIVING annuities. If you missed it, please go back and read that first so you can get ALL the information on ALL the options available to you. This post though, is dedicated to GUARANTEED annuities.

Essentially, it’s an insurance product. You give your retirement savings over to an insurance company and they guarantee to pay you an income for the rest of your life. If you’ve been employed and you earned a salary every month, this is very similar. You don’t need to worry or even think about what returns the market is giving, your income is set and guaranteed.

Let this just sink in – this salary will be paid to you FOR THE REST OF YOUR LIFE. If you live to 120 years, well – well done! You’re still receiving a salary.

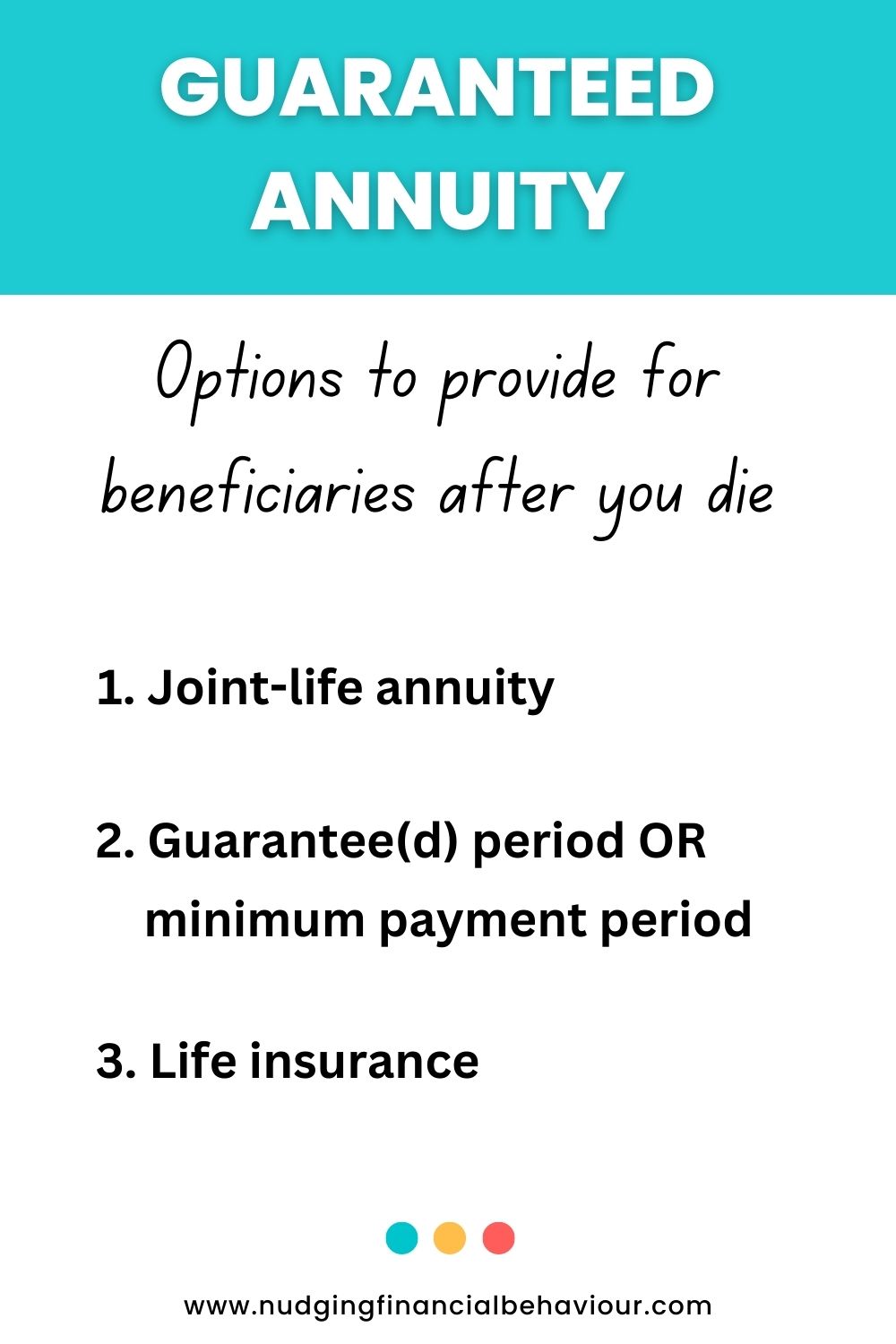

But now you’re probably thinking about the other side… what if you die at 70? The insurance company keeps all the retirement savings you gave to them? Yes… and No? There ARE options available that ensure your money will continue being paid to your partner and beneficiaries after you die… we unpack those in detail in the video that follows.

We also discuss a very important number to look out for when purchasing a guaranteed annuity: your starting income:

The nice thing about a guaranteed annuity is that you just never need to worry. No matter what happens in the markets, no matter how long you live, you’ll never be without an income.

This is an important consideration because essentially the need to make complex financial decisions is taken out of your hands. We should never underestimate the risk of getting dementia in old age. Or our partner getting dementia. That limits our ability to make complex decisions.

Now that you understand what a guaranteed annuity is, the next thing to consider is that there are different types of guaranteed annuities… that’s what we’ll be covering in the next post.

If you haven’t done so yet, subscribe to our YouTube channel.

Want to pin this post for later?

Dr Gizelle Willows

PhD and NRF-rating in Behavioural Finance