January always arrives with a strange emotional weight. After the noise, generosity and spontaneity of December, the first month of the year feels quiet, stretched, and financially demanding. Bank accounts are still recovering from December overspending, debit orders feel heavier than usual, and payday seems impossibly far away.

The truth is that January isn’t a financial crisis, it’s a behavioural one. And once we understand the psychology behind this month, we realise it doesn’t need to be feared. It just needs to be navigated.

Part of January’s emotional toll comes from a shift in how our brains interpret money before and after the holidays. December is full of heightened emotion — excitement, generosity, nostalgia — and these emotional states encourage present bias. We tell ourselves that “it’s just once a year” or “I’ll deal with it next month,” and December-you happily obliges.

Then January arrives, and suddenly the same purchases feel irrational. This isn’t because you made terrible decisions, it’s because January-you and December-you are not operating from the same psychology.

Even though this level of spending on Black Friday and in December isn’t sustainable, it becomes a mental anchor. So when January returns to normal, it feels like a loss. Not because things are worse, but because your reference point shifted.

This is why post-holiday financial stress feels so real, even when the numbers aren’t dramatically different from other months.

Understanding the psychology is helpful, but what people really want to know is how to make your money last until payday and what to do when January feels financially overwhelming.

Here is a behavioural approach that genuinely works:

Trying to “survive January” as one long block makes the month feel endless. A more behaviourally intelligent approach is to break it into segments, what we call micro-weeks. Instead of planning for the rest of the month, plan only for the next five or seven days. Breaking goals into smaller, manageable units has been shown to significantly reduce anxiety and increase follow-through, because short planning horizons feel more achievable to the brain.

This reframes the experience. Suddenly January is no longer a marathon; it’s a series of short, achievable stretches. The pressure eases, panic reduces, and your sense of control increases.

Small deeds done are better than great deeds planned.

January is the month where willpower is at its lowest. Routines are restarting, work resumes, schools reopen, and decision fatigue is real. This is exactly when relying on discipline is least effective.

That’s why pre-decisions help so much. When you decide in advance how you’ll behave, you free yourself from daily negotiation. Behavioural researchers have shown that reducing decision fatigue by relying on pre-commitments dramatically improves self-control and financial outcomes.

You do not rise to the level of your goals. You fall to the level of your systems.

You might:

These aren’t rigid rules, they’re calming anchors. They reduce temptation by removing the need for constant decision-making.

One reason December overspending sneaks up on us is because buying becomes effortless. One tap. One click. One “Add to Cart.”

January benefits from the opposite: spending that is just a little harder.

You can:

This tiny bit of friction interrupts impulse purchases. It creates just enough space to think, “Do I really need this?” And often, the answer is no.

Many people try to make January survivable by cutting out all pleasure. Ironically, this backfires. When you experience emotional deprivation, you’re more likely to overspend in February as a rebound.

What works better is replacing expensive joys with low-cost ones. January needs affordable dopamine.

Examples might include:

These small comforts keep your mood stable and decrease the psychological heaviness of the month, without straining your budget.

The best things in life are free. The second-best are very expensive.

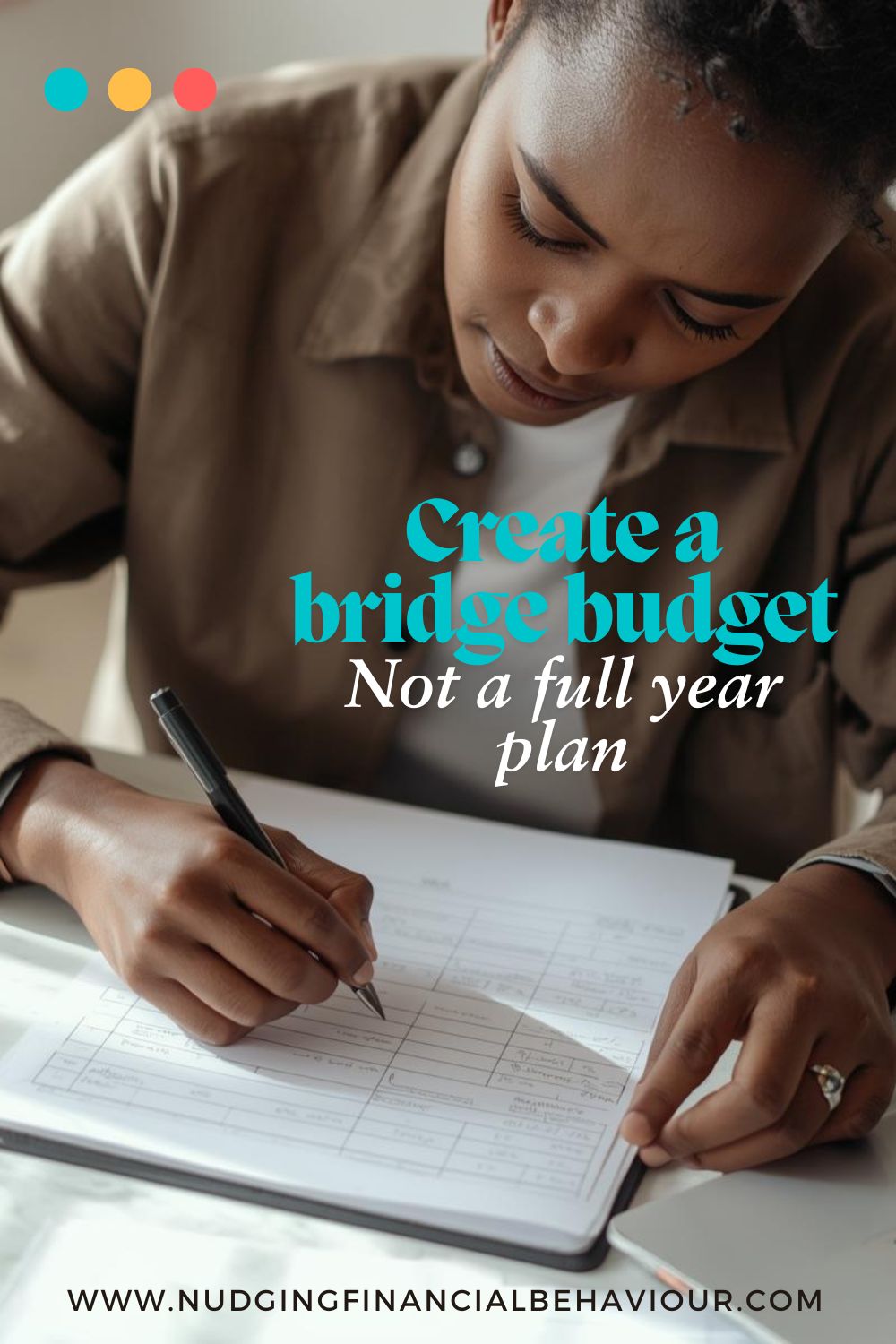

January is the worst month to attempt an annual budget. Your brain is overloaded, and your motivation is inconsistent. What you need isn’t a 12-month spreadsheet, it’s a simple bridge from now to payday.

A bridge budget asks only:

“What do I need to get through the next two weeks?”

You identify essentials, keep one or two comforts, and temporarily pause non-urgent costs. This is a compassionate, behaviourally aligned way of stabilising the month.

Perhaps the most important reminder is that January is not a verdict on your financial discipline. It is a predictable psychological dip after an emotionally charged, financially heavy month. You are not failing; you are adjusting.

If December was a time of emotional generosity, let January be a time of behavioural gentleness. Be curious, not critical. Ask yourself what you might do differently next year, instead of berating yourself for what you didn’t do this time.

With the right behavioural tools, January becomes manageable, even survivable. And by the time February arrives, you’ll look back and realise:

You didn’t just get through the longest month of the year.

You understood it, navigated it, and walked out steadier than before.

This too shall pass.

Dr Gizelle Willows

PhD and NRF-rating in Behavioural Finance