This post considers risk aversion vs loss aversion. Now that we understand framing, we can look at the impact of framing different decisions as either a gain or a loss. You’ll learn what it means to be risk averse and discover how behavioral economics and science strips that down into an incredibly powerful bias known as loss aversion. This then touches on prospect theory, the disposition effect and finally, impression management.

If the same choice is framed as a loss, rather than as a gain, different decisions will be made. This introduces the concept of risk aversion and loss aversion. Two terms that are often thrown around when discussing our tolerance for risk. While they might sound like the same thing, they’re actually very different things. While risk aversion refers to where we value gains and losses equally, loss aversion refers to where we value losses more than gains. That’s loss aversion vs risk aversion.

Consider that you are offered the following bet. On the toss of a fair coin, if you lose you must pay $100. What is the minimum amount that you need to win in order to make this bet attractive to you?

Is it $100? $150?

If you choose an amount that is more than $100 you’re displaying loss averse behaviour.

If we valued gains and losses equally (risk aversion) then we would be willing to enter the bet with a 50% chance of winning or losing $100 i.e. we’re attributing the same value to losing $100 that we would to gaining $100.

However, if you’re asking for more than $100, then you need to be compensated with a higher potential gain to justify the loss. Why? Because the losses are more painful.

A good example of this was a study of a campaign promoting breast self-examinations (BSE). Two different pamphlets were handed out to women. Pamphlet A stated: “Research shows that women who do BSE have an increased chance of finding a tumour in the early, more treatable state of the disease.” Pamphlet B stated: “Research shows that women who do not do BSE have a decreased chance of finding a tumour in the early, more treatable state of the disease.” The study showed that pamphlet B (framed as a loss) created significantly more awareness and BSE behaviour than pamphlet A (framed as a gain).

What I’m hoping I’m succeeding in showing you with all these real world examples of loss aversion vs risk aversion is that we make decisions based on the value of potential losses and gains, rather than the outcome.

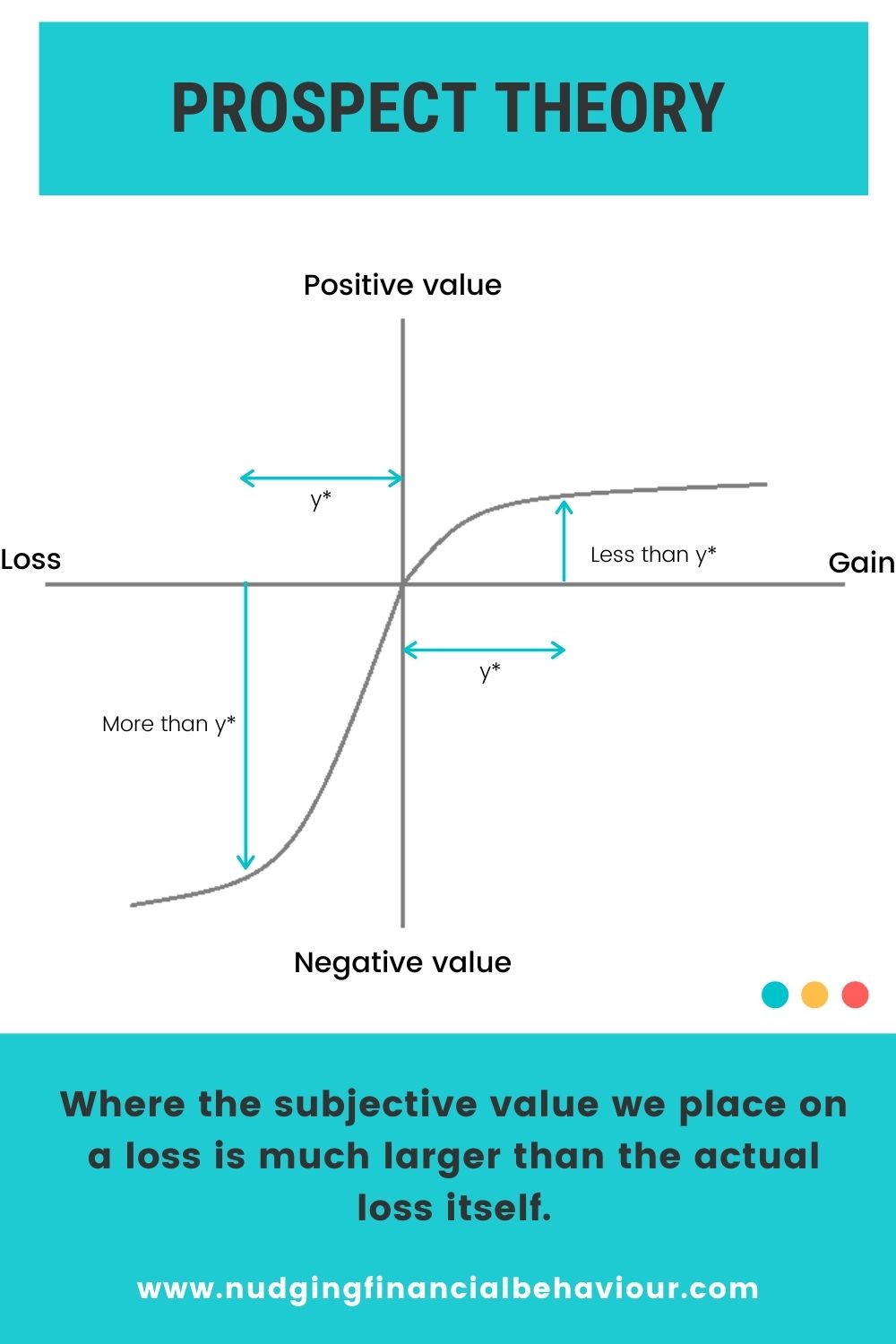

For those that understand things better with pictures, the following graph explains a theory known as prospect theory. It was developed by Nobel Laureate and behavioral economist Daniel Kahneman and Amos Tversky.

The horizontal axis measures the value of our gain and loss, whilst the vertical axis measures how we value that gain or loss.

Looking at the horizontal line (shown as y) on the right-hand side of the graph, it shows the objective value of a certain gain. The vertical arrow pointing upwards reflects the subjective value we attach to this gain. The observation to take note of is that the subjective value we place is less than the actual objective gain.

Looking at the other horizontal arrow (measured at the same value, i.e. y) on the left-hand side of the graph, it shows the same value, but this time as a loss. The vertical arrow pointing downwards is longer than the horizontal arrow, showing that the subjective value we attach to this loss is much larger than the actual loss itself.

If a gain or a loss, was $100 it shows that we place a larger value on a loss of $100, than on a gain of $100.

Put simply, losses loom larger than gains Share on XEven Tiger Woods suffers from this….

An experimental study was performed to measure the presence of this fundamental bias we now know as loss-aversion, in a high-stakes context: professional golfers’ performance on the PGA TOUR. As we know, golfers are scored according to the number of strokes they take during a tournament, yet each hole has a salient reference point, known as par.

1.6 million putts were analysed using precise laser measurements and it was found that golfers play better when attempting to avoid dropping a shot than when trying to gain one, when they consistently leave their shots short. In relative terms, golfers were equating a ‘bogey’ to a ‘loss’, and a ‘birdie’ to a ‘gain’.

In economic terms, this loss-aversion on the part of professional golfers was measured and found to equate to $1.2 million in tournament winnings per year.

Time to discuss the difference between risk aversion and loss aversion attitude of investors. If you’re an averse investor, you might have already heard about something referred to as the disposition effect. It’s the manifestation of loss aversion in our investing decisions. When we hold a share that has made a loss, we tend to continue holding it. But when we hold a share that has made a profit, we tend to sell it.

Consider the words of 16th century political scientist, Niccolo Machiavelli:

Do all the harm you must at one and the same time, that way the full extent of it will not be noticed, and it will give least offense… One should do good, on the other hand, little by little so people can fully appreciate it.

This is popular mechanism used in earnings announcements and there’s a whole field of study, known as impression management, which uses such subtleties to make you ‘feel better’ when reading earnings announcements and annual reports. From overloading you with information around things they don’t want you to understand, to using symbols rather than words for things they want to draw your attention to. And finally, using prospect theory and drip feeding the good news throughout the report so that you almost forget about the bad news that was 20 pages earlier. I’m not saying this practice is wrong. I’m saying it’s clever. But I’m also saying that as consumers, we need to be aware of it.

Furthermore, the understanding of loss aversion shouldn’t be limited to impression management. If as a company you pay out bonuses once a year – consider taking that same bonus and dividing it up into smaller mini-bonuses throughout the year. Prospect theory tells us this practice will maximise the utility received by employees.

Want to pin this post for later?

Dr Gizelle Willows

PhD and NRF-rating in Behavioural Finance

Understanding the power of how information is displayed to you can really help you when it comes to future financial decisions. A good example of a product designed to take advantage of the behaviours attached to loss aversion are insurance policies. If we are loss-averse and make decisions to avoid potential losses, then insurance products are perfect for us. They are designed to highlight the potential loss. This then

Understanding the power of how information is displayed to you can really help you when it comes to future financial decisions. A good example of a product designed to take advantage of the behaviours attached to loss aversion are insurance policies. If we are loss-averse and make decisions to avoid potential losses, then insurance products are perfect for us. They are designed to highlight the potential loss. This then

Have you ever considered publishing an e-book or guest authoring on other blogs? I have a blog based upon on the same subjects you discuss and would love to have you share some stories/information. I know my visitors would enjoy your work. If you are even remotely interested, feel free to shoot me an email. Alonzo Lacks